- It appears MFIN was forced to deplete its holding company cash balances to repay $31.25 million in debt

- The Company tried and failed to raise debt before the February 26th, 2026 maturity

- MFIN will need to raise debt or equity SOON – we believe it will be expensive or one-sided

- This situation is DIRECTLY A RESULT OF poor management and no board oversight

- Markets are afraid in general, MFIN’s decision-making is making it worse

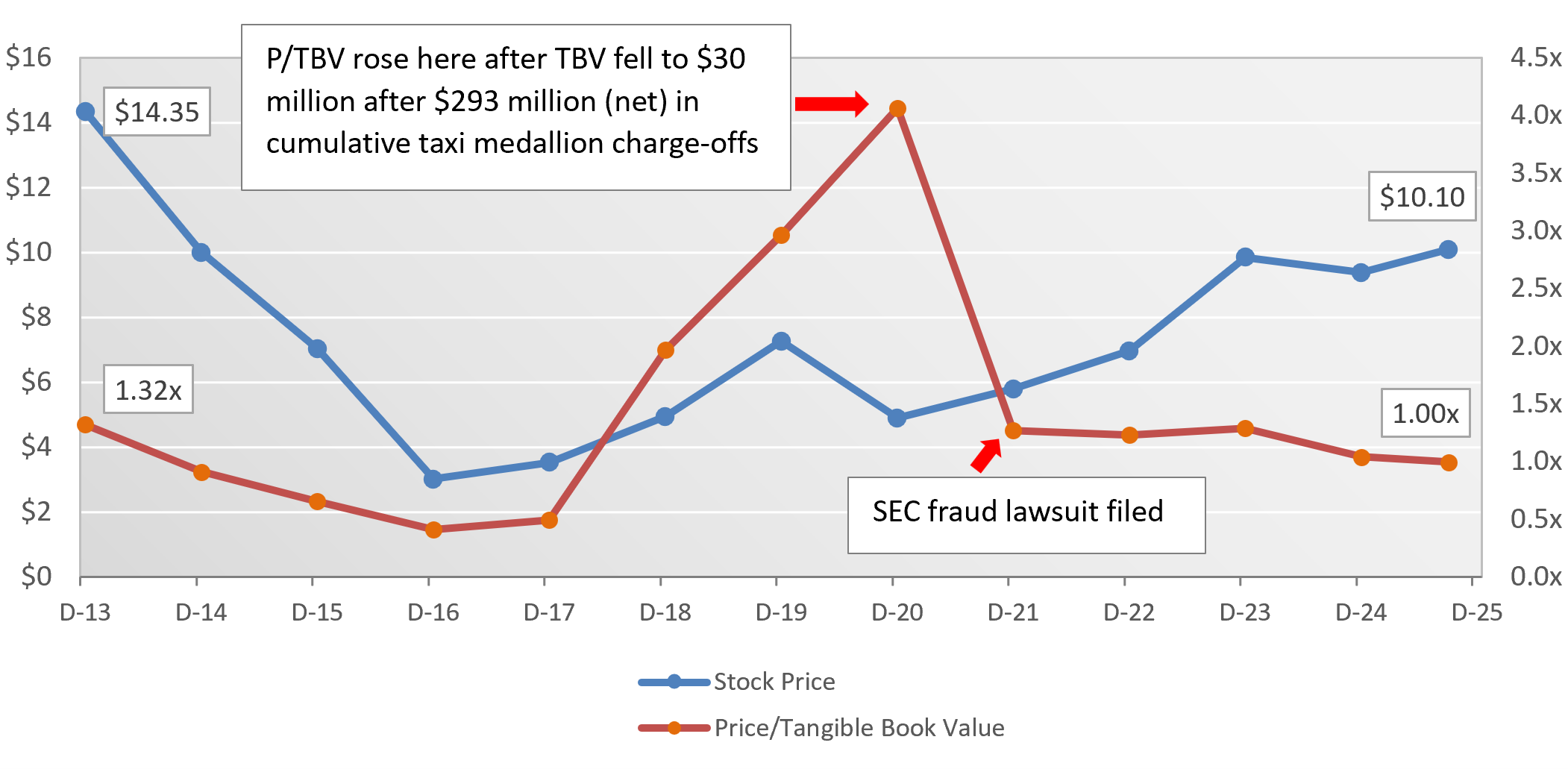

- MFIN’s Tangible Book is still below its 4Q2013 peak - stock price is down 40% from its peak

- Price/Tangible Book Value is a terrible ~1.0x and substantially below other lenders and MFIN-selected peers

- MFIN needs better leadership and a tech-first mindset to succeed

MINNEAPOLIS, March 06, 2026 (GLOBE NEWSWIRE) --

ZimCal has put together a short presentation (here) that shows why the recent debt maturity and paydown is just more evidence of serious underlying issues with MFIN’s leadership. The Company is being held back by poor decisions and low institutional investor confidence. We believe MFIN was forced to deplete its holding company cash reserves to repay $31.25 million in maturing debt – and we believe this could have been easily avoided.

ZimCal Asset Management LLC (“ZimCal”, “We”, “Our”) believes Medallion Financial Corp. (“Medallion”, “MFIN”, the “Company”) is undervalued and is being held back by poor leadership.

We have been invested for 5 years and have analyzed every release, note purchase agreement, SEC filing, employment contract, etc.

ZimCal’s principal has invested in lenders and banks for over 15 years. We have NEVER publicly criticized a firm but felt we had no choice with MFIN. We believe our investment would be worth substantially more if Medallion had the right leadership and business strategy.

During 2025, we approached the Company and its board privately, sharing our concerns, suggestions and offering assistance - and we were ignored. A more public approach is one of the few remaining options.

Medallion tried AND FAILED to raise debt prior to the maturity of its $31.25 million senior notes and appeared to use cash reserves to repay it since no debt terms were announced in its Form 8K. MFIN has likely depleted its cash reserves at its holding company and it CANNOT legally use cash balances at Medallion Bank to directly repay holding company debt. Medallion will have to either take more money out of the Bank (reducing growth and profitability) or raise (expensive) debt or equity. It will need to do so soon: we expect by quarter end. It can possibly defer this by taking money out of its commercial lending SBIC, but that is a band-aid and will not stop the inevitable.

MFIN has huge potential. Its subsidiary, Medallion Bank, is a solid platform making solid profits but is being bled dry by tens of millions in executive pay and high corporate costs at its holding company. Many investors are staying away from Medallion because they don’t trust management and are repelled by the stink of the SEC fraud lawsuit against Medallion’s current CEO. If MFIN’s leadership is improved, this can be corrected very easily, and all stakeholders (including us) would be rewarded.

But first, a quick recap for those that don’t know the background.

- In early 2010s, Medallion made really bad taxi medallion loans to weak borrowers

- Uber and Lyft began destroying the taxi medallion business

- Risks were obvious and alarms came from external (banks, Bloomberg, Vox, and others) and internal (executives) sources – but Andrew Murstein (the current CEO) ignored them

- Instead, Murstein paid contractors to publish over 100 bogus “research” pieces and post 900+ comments online on Seeking Alpha etc. to pump up Murstein/Medallion and attack critics

- Murstein repeatedly inflated the value of Medallion’s assets to show profits

- Murstein allegedly lied to Medallion’s auditors (who have since resigned)

- Medallion wrote off almost $300 MILLION in bad loans in 4 years. Tangible book value dropped below $30 million and the stock fell to under $2/share

- MFIN stock is now at $10/share but at a terrible 1.0x Price/Tangible Book and after 12 years, still far below its peak 2013/2014 tangible book (15% down) and stock price (40% down)

Despite recent profits, MFIN’s stock price is ~40% below peak and TBV is less now than it was in 2013

Price/Tangible Book is weak at ~1.0x and well below peers: YE 12/31/13 – 3Q25 Data

| Source: FDIC UBPR and S&P Capital IQ - MFIN stock peaked at $17.74 on 11/19/13 and YEAR-END TBV peaked at ~$270 million |

Murstein was sued by the SEC for securities fraud (see all the bullet points above) and all legal fees to defend him and $3 million in SEC penalties were paid by stockholders, not Murstein. In the meantime, Murstein’s family and friends on Medallion’s board gave him over $20 million in bonuses, country club membership, a company car and a personal driver. His bonuses can be clawed back by the board and would add almost 10% to Medallion’s market cap, but the board refuses to do anything. This is because 3 of 8 directors are Murstein family members, the average director tenure is 18 years (including Medallion Bank) and 5 of the 8 board members are 80+ years old. There has been no accountability for Murstein – in fact, he was recently promoted to CEO and is being paid much more than peers that have consistently outperformed Medallion.

If Medallion wants to act like a family business and pay huge bonuses for declining performance, they should go private. The Company has tried to buy stockholder support by raising dividends but that’s forced them to add $42 million in expensive liabilities in the last 2 years to pay for it. Performance in Medallion’s core consumer book (95% of its loans) is poor and declining (low ROAA, ROAE and increasing bad loans in Recreation). The Commercial Lending segment has shown ~20% non-performing loans over the last 3 quarters. Medallion has used one-off shenanigans, timely recoveries from a discontinued business and unpredictable “gains” to pad EPS and hide poor management decisions.

Under the right leadership, this could all be turned around instantly, and value could be unlocked.

See our accompanying presentation to see how Medallion could improve and reward its stakeholders – ideas we shared with Medallion privately almost 2 ½ years ago and that we have shared privately and publicly several times since. But rather than face the obvious and engage, they ignored and attacked. Just like they did ten years ago. Not unexpectedly, they’ve also taken some of our ideas they dismissed publicly and passed them off as their own...We’ll take it. We want improvements – not credit.

Our singular focus is on making MFIN better and more valuable, which will make our investment more valuable.

About ZimCal Asset Management, LLC

ZimCal Asset Management is an alternative investment firm focused primarily on niche, illiquid and complex credit investment opportunities.

ZimCal Asset Management partners with both healthy and distressed borrowers or issuers and provides customized solutions that meet their unique needs and circumstances. Over the last 15 years, the founder of ZimCal Asset Management has developed a specialization investing in FDIC-insured institutions and has partnered with over 120 bank lenders through investments on both sides of the balance sheet.

ZimCal usually works in collaboration with bank leadership teams and if required, but on very rare occasions, will insert itself more forcefully if it believes that leadership is underwhelming and threatens to undermine stakeholder investments. ZimCal prides itself on performing extensive, rigorous financial analysis and research to fully understand the risks of any investment.

Important Information and Disclaimer

ZimCal Asset Management, LLC, and its affiliates BIMIZCI Fund, LLC, and Warnke Investments LLC (collectively, “ZimCal” or “we”), are, directly or indirectly, owners of securities of Medallion Financial Corp. (the “Company”). ZimCal currently beneficially owns shares of common stock and Trust Preferred securities. You should assume that ZimCal may from time to time sell all or a portion of their holdings of the Company in open market transactions or otherwise, buy additional shares (in open market or privately negotiated transactions or otherwise), or trade in options, puts, calls, swaps or other derivative instruments relating to such shares. We are not currently engaged in any solicitation of proxies from stockholders of the Company. ZimCal intends to monitor the performance and corporate governance of the Company, as well as the actions of the Company’s management and Board. As ZimCal deems necessary, ZimCal will assert its stockholder rights.

Except as otherwise set forth herein, the views expressed reflect ZimCal’s opinions and are based on publicly available information with respect to the Company. We recognize that there may be confidential information in the possession of the Company that could lead it or others to disagree with our conclusions. ZimCal reserves the right to change any of its opinions expressed herein at any time as it deems appropriate and disclaims any obligation to notify the market or any other party of any such change, except as required by law. We disclaim any obligation to update the information or opinions contained herein.

The information herein is being provided merely as information and is not intended to be, nor should it be construed as, an offer to sell or a solicitation of an offer to buy any security.

Some of the information herein may contain forward-looking statements. All statements contained herein that are not clearly historical in nature or that depend on future events are forward-looking. The words “anticipate,” “believe,” “expect,” “potential,” “could,” “opportunity,” “estimate,” “plan,” and similar expressions are generally intended to identify forward-looking statements. There can be no assurance that any forward-looking statements will prove to be accurate and therefore actual results could differ materially from those set forth in, contemplated by, or underlying these forward-looking statements. In light of the significant uncertainties inherent in forward-looking statements, the inclusion of such information should not be regarded as a representation as to future results or that the objectives and strategic initiatives expressed or implied by such forward-looking statements will be achieved.

An infographic accompanying this announcement is available at https://www.globenewswire.com/NewsRoom/AttachmentNg/2b6e4067-7c30-4aa4-9ff4-0c32da9a4fa2

Media contact: nicole@nh-consult.com